A beginner's guide to accounting fraud (and how to get away with it): Part III

Paper chafe

We’ve spent a fair bit of time talking about fake revenue and how to hide it. But don’t get the wrong idea, we have a real product to sell here. We’re in the business of convincing people to buy new stock in our company. As in, they give us pieces of paper with someone’s head on it. Benjamin preferably, but I’d settle for the Lizzy (or even a generic bridge). In return we offer them another piece of paper, one that has our word behind it. That’s how we get our cashflow.

The trick, I think, is having a story that people don’t want to admit that they don’t understand. And we want to be able to say we have a really, really big total addressable market. Lots of blue sky. As in we might be able to sell a lot of product, one day. That way it could just be true that our paper actually is going to be worth a lot more than the paper they gave us, this time next year...

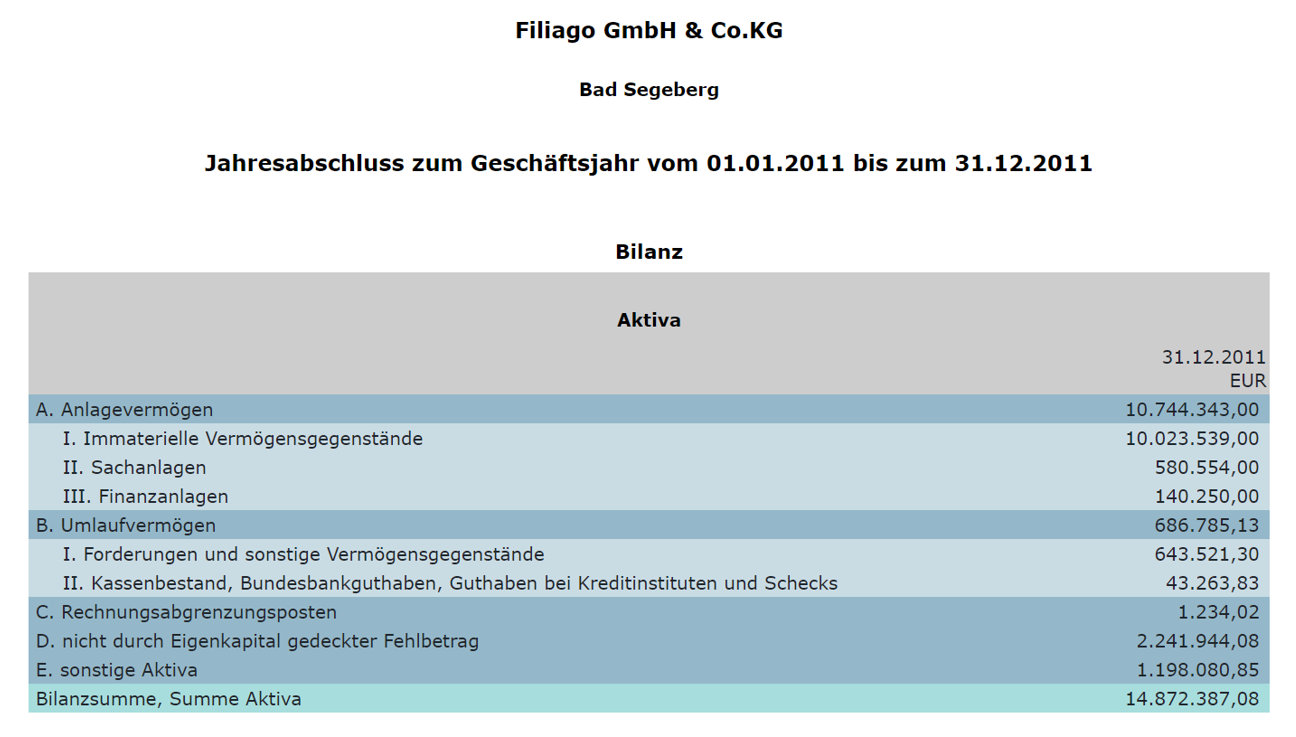

If you’re looking for a role model for how to serially raise capital for a business that really shouldn’t even exist in the first place, you could do a lot worse than Avanti Communications. Avanti was a startup satellite broadband operator that issued half a billion odd of equity, and about as much again in debt, in just five short years. No one seemed to care much that the business case was flawed from the start. That revenue kept falling short and customers got less and less substantial. And, of course, it didn’t matter that the accounts read like a Stephen King novel. Because you can’t get a bigger addressable market than space, can you?

How did I know Avanti was always bound to end up failing its shareholders, even before it took off? The company said so. In black and white. It told me and every other investor that bothered to look at its 2009 annual report. I know corporate filings aren’t exactly gripping but it helps if you read them. Lucky for us, it doesn’t seem like many people do.

When I‘d asked directly, management had flat out refused to disclose what the Mb capacity of its first satellite (called Hylas-1) would be “for commercial competitive reasons”. But they soon went ahead and gave it away in a press release anyway, stating that 320Mb was about 10% of the total. From there it was simple to estimate build cost per Mb, which came in around £35mn. The problem was Eutelsat, which was about to launch its own broadband satellite over Europe too. This bird, KA-SAT, was 15 times as big but only cost about 3 times as much to build. It’s unit cost was more like €4mn per Mb. That was going to be an issue for Avanti.

Don’t take my word for it, take the company’s. In its 2009 annual report Avanti already states that Hylas-1 “will be full with around 200,000 - 300,000 end user customers”, with the higher number only possible if it delivered a lot of them something not much better than a Netscape dial-up service (as in 0.5Mb per second). But even then Eutelsat had a 3.6Mb per second product in the market, for €17 a month wholesale. And had said publicly it would be keeping that price point once KA-SAT was up, but for a 10Mb per second service. Hylas-1 was going to be competing with that, but at those speeds it would be able to serve a lot less customers. It’s not quite a straight line calculation because of contention - basically congestion from other users – but it wasn’t good news for Avanti. Commercial wholesale revenue for Hylas-1 would end up end peaking at around €15mn while sell side consensus was still “modelling” four times that.

When I tried to talk this through with the company the call went nowhere. Investor relations claimed the annual report didn’t say what I thought it did (I always liked to send over my questions ahead of a meeting, so they knew what I was talking about). They were so sure, in fact, that they said they hadn’t even bothered to go back and check the wording. So I read it over the phone - it’s on page 13 if you want to take a look for yourself - and that was pretty much the end of the call.

Thinking about Avanti reminds me of meeting Simon Cawkwell. My boss had suggested I get in touch as he was one of the only short sellers in the UK with a big profile at the time, under the pseudonym Evil Knievel. He’d even written a nice little book on shorting:

Lunch at his flat was quarter inch thick slices of salami and several bottles of red wine (there might have been bread too). I definitely talked him through why I was short Avanti. We never met again after that because he was a walking invitation to a defamation lawsuit (as well as a coronary). To be honest I don’t even know if he’s still alive. Back then he didn’t look like he should be, but I hope he’s well. He had a great talent for seeing when balance sheets didn’t make sense, even through all the wine.

I mention Simon because defamation law is really useful when you’re in the fraud business. And that brings me on to the point of this digression. We need to think about where we want to do what we want to do. I already said our real product is our company’s paper currency. Our stock. So for starters we need to be somewhere with a liquid equity market. Somewhere with plenty of willing buyers. Retail mugs investors tend to be best. To hook them we need a stock market listing in a rich country, where plenty of people have more money than sense.

Still, not all these markets will treat us as well as job-creating entrepreneurs such as ourselves deserve. As in, we want as little disclosure as possible. The United States is not great for starters. It has this childish ideal they call free speech. I used to think that was a bit of a gimmick, like when the Yanks claim to have invented liberty and democracy (as long as you weren’t three fifths of a human being, obv). But when it came to shorting it really did make a big difference. The operating principle of the First Amendment is, basically, so long as you believe what you are saying is true, you can say it. So you say a lot. The legal precedent of British defamation law is that, unless you can definitively prove what you’re saying is factually correct, you are going to be out of pocket. So you don’t say much. Isn’t that great for us?

To be fair the UK does have an aggressive, independent fourth estate, and that undercuts some of the advantage we would get from hiding behind defamation law. I’m not saying that because the FT paid me. It didn’t. I’m saying it because the FT seems to be immune to corruption. I couldn’t even blag a table at the Alphaville quiz night. But I guess that’s not important…

Some years into the long and winding cash bonfire that was Avanti Communications, I got a call out of the blue from Matt Earl. I don’t think we’d ever spoken before (but this was, chronologically, after lunch with Simon Cawkwell, so maybe my memory is hazy). I knew of Matt though, and he knew Simon well. He had a reputation for calling structural shorts in the support services sector; names like social housing contractor Connaught.

Matt wanted to talk to me about something he’d spotted in Avanti’s recent numbers. I don’t have time to go into detail here, but how the company managed to lend £9.1mn in cash to a small prospective customer in Germany in the first half of 2011, then take it over when it defaulted the same November, and yet end the year with next to nothing tangible to show for it is beyond me. I get Filiago was losing money, but nowhere near that much, so where did the readies go?

I liked this story so much I started using the question as part of my interview process for new hires. Answers on a postcard please. No doubt there is a genuine explanation out there but I have an idea about how we could use something similar to help us too. That’s for another post though.

The next time I heard of Matt after that was when he was outed as one of the principals of Zatarra Research. Zatarra had published a report suggesting criminal links to Wirecard’s operations. I wasn’t that taken with the report then. I’d already come across a lot of the connections it highlighted, and I’d discussed them with Dan McCrum back in 2014. So I wasn’t surprised they eventually surfaced. I’m not interested in talking about the report now either. What’s interesting for us was the reaction of the German regulator Bafin, which thought the right response was to go after the authors and threaten to prosecute them. A few years later it decided to give FT journalists the same treatment. This is the kind of proactive oversight a business like ours could really use. The fact that the German parliamentary committee investigating Wirecard’s collapse felt the need to apologise a few years later is nice for Matt, I guess, and exactly the level of belated token gesture we want to see regulatory action reaching.

We also want to be in a place where it’s not so obvious we are making this up as we go along. I always found it interesting that a lot of stock promotions are listed on equity markets that are not in the countries where they actually operate. It’s a good idea. We want our investors as far away as possible from where we are claiming to do business. Like a Kentucky iodine plant listed in London. Around 2010 a long line of Chinese firms (and a few US brokers) made an art form of this, and the careers of a few short sellers. For us, I like the sound of Canada, but I’ve heard good things about Australia too.

Balancing all these needs isn’t easy. Do we want a cosy relationship with a regulator or a big troop of willing punters more? Or is it better to just be able to silence critics with a letter from our lawyer?

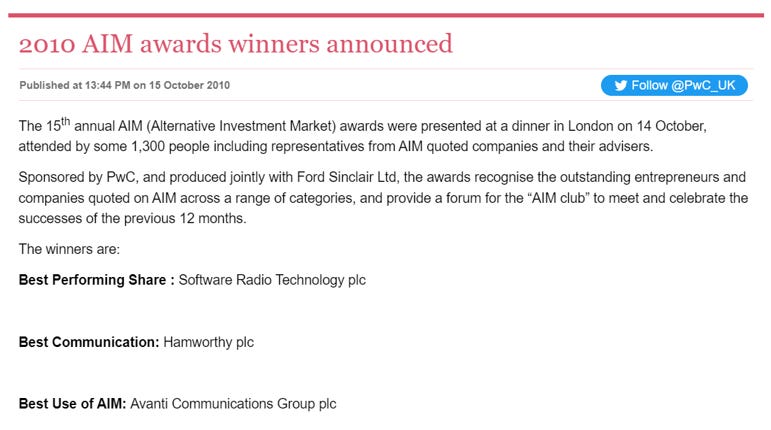

I guess if I had to choose just one point in spacetime for us to do this fraud it would probably be on the UK’s Alternative Investment Market (AIM) in March 2014. I mean when the five largest stocks include Monitise, Gulf Keystone and, of course, Quindell, who’s going to look at us funny?

In 2010 Avanti won an actual award for “best use of AIM” :

It’s hard to argue management didn’t deserve this but the best thing for Avanti owners would have been if its satellites blew up on launch. At least that way they would have got an insurance payout at build cost. No such luck. Avanti did blow up though. One more black hole in the equity space.

As for the paper its shareholders got for their money, well let’s just say it would have been worth more during lockdown.

Amazing work Leo!! Absolutely love your writing style you have a serious gift! (Is that what your studying at OU?)

I also bought the Simon Cakwell book but fkme it’s dull. Could never get round to finishing it. My pops had another book bh him (used to be his stockbroker lol) a book about Rupert Murdock!Might be worth something now. ££

This is a wonderful piece. It does make me want to explore which countries are offering the best environment for fraud today.

But maybe the real opportunity today is not in the private sector. hmmm.